When Is the Right Time to Invest in a Retirement Community?

Deciding when to move into a retirement community isn’t just about age—it’s a financial turning point. Many people wait too long, missing key benefits, while others jump in too early and tie up their assets prematurely. I’ve seen firsthand how timing impacts everything from cash flow to lifestyle freedom. This decision blends personal readiness with smart financial planning. So, when should you act? Let’s break down the real factors that signal it’s the right time—without hype, just clarity.

The Financial Crossroads: Recognizing Your Retirement Readiness

Transitioning into a retirement community is more than a change of address—it’s a strategic financial decision that hinges on long-term stability, not just immediate affordability. True readiness goes beyond having a lump sum saved; it involves assessing whether your income can sustainably support monthly fees, healthcare costs, and unexpected expenses over decades. For many families, the ideal moment arrives not at a specific age, but when their current living situation begins to drain resources rather than preserve them. A home with rising maintenance costs, property taxes, and utility bills may no longer serve as an asset—it can become a liability. When housing expenses consume more than 30% of retirement income, it’s often a warning sign that a shift is needed.

One of the most overlooked indicators of financial readiness is income predictability. Retirees who rely on consistent sources such as Social Security, pensions, annuities, or dividend-paying investments are better positioned to handle fixed monthly charges associated with senior living. In contrast, those dependent on fluctuating investment returns or part-time work may face uncertainty that complicates long-term commitments. Equally important is debt load. Individuals carrying significant mortgage balances, credit card debt, or personal loans may find themselves stretched too thin if they add another layer of recurring expenses. Reducing or eliminating high-interest debt before making the move can dramatically improve financial flexibility and peace of mind.

Another critical factor is healthcare forecasting. While many retirement communities offer tiered care options, understanding future medical needs helps determine which level of service is appropriate—and affordable. Waiting until health declines sharply can limit choices, force rushed decisions, and result in higher entry fees due to increased care requirements. Proactive planning allows individuals to select communities based on preference rather than necessity, often securing better value and access to preferred amenities. Those who assess their health trajectory early—factoring in family history, chronic conditions, and mobility trends—can align their financial strategy with realistic care expectations, ensuring their savings last as long as they do.

Finally, asset liquidity plays a central role in determining readiness. Selling a home is typically the primary funding source for retirement community entry, but this process takes time. Markets fluctuate, and unexpected delays can disrupt timelines. Having accessible funds to cover initial deposits or bridge gaps between sale and move-in provides crucial breathing room. Retirees who wait until every dollar is committed elsewhere risk losing negotiating power or being forced into less desirable arrangements. The goal is not to act impulsively, but to recognize when financial conditions align—when income is stable, debts are low, healthcare needs are foreseeable, and assets can be converted efficiently. That convergence marks true readiness.

Upfront Costs vs. Long-Term Value: What You’re Really Paying For

At first glance, the price tag of a retirement community can seem steep—especially when entry fees range from tens of thousands to over a hundred thousand dollars, plus ongoing monthly charges. However, viewing this expense in isolation misses the bigger picture. What retirees are actually purchasing is a bundled package of services and peace of mind that would otherwise require separate budgeting, coordination, and management. These include home maintenance, landscaping, utilities, security, housekeeping, meal plans, social programming, and access to healthcare monitoring. When broken down, the per-service cost often compares favorably to what individuals pay independently to maintain a private residence.

Consider the hidden expenses of aging in place. Homeownership comes with inevitable upkeep—roof repairs, HVAC replacements, plumbing fixes, and accessibility modifications like stairlifts or bathroom renovations. According to national housing data, homeowners over 65 spend an average of $3,500 annually on maintenance alone, with costs increasing as properties age. Add to that property taxes, insurance premiums, utility bills, and lawn care, and the total annual burden can easily exceed $10,000—even without major renovations. In contrast, most continuing care retirement communities (CCRCs) bundle these services into a single predictable fee, shielding residents from surprise costs and eliminating the need to source contractors or manage projects.

Beyond cost savings, there’s value in time and mental energy. Managing a household requires physical effort and decision-making—tasks that become more challenging with age. For someone dealing with early mobility issues or cognitive changes, even small chores like changing light bulbs or organizing bills can become sources of stress. Retirement communities alleviate these burdens by providing structured support, allowing residents to redirect their focus toward relationships, hobbies, and well-being. This intangible benefit—freedom from daily hassles—is difficult to quantify but deeply meaningful in quality-of-life terms.

Moreover, many communities offer scalable care options. A resident might begin in independent living, transition to assisted living, and eventually receive skilled nursing—all within the same campus. This continuity avoids the emotional and logistical strain of multiple relocations during health decline. While not all contracts guarantee lifetime care, those that do (often called Type A or life-care contracts) provide a level of security unmatched by standalone insurance policies. Though these models come with higher upfront fees, they protect against the soaring cost of long-term care, which can exceed $100,000 per year in some regions. By pre-paying for potential future needs, retirees effectively hedge against one of the largest financial risks in later life.

Timing the Market: How Real Estate Trends Affect Your Move

The decision to sell a home and move into a retirement community is inextricably linked to real estate market conditions. The timing of the sale can significantly impact available capital, influencing both the range of communities one can afford and the level of financial security in retirement. Selling during a peak market can generate substantial equity, enabling access to premium facilities with refundable entry fees or enhanced care packages. Conversely, exiting during a downturn may leave sellers with insufficient proceeds, forcing compromises on location, amenities, or care levels. Therefore, monitoring regional housing trends and understanding local demand dynamics is essential for maximizing returns.

Regional variation plays a major role. Some areas have experienced sustained appreciation due to population growth, limited housing supply, or strong job markets, while others face stagnation or decline. Retirees in high-appreciation zones may benefit from waiting a few years to capture additional gains, provided they can manage ongoing ownership costs. In slower markets, however, delaying could mean missing the best available pricing. Working with a knowledgeable real estate advisor who understands senior transitions can help identify optimal windows for listing, staging, and negotiating. Additionally, preparing the home for sale well in advance—through decluttering, minor upgrades, and energy efficiency improvements—can enhance marketability and attract competitive offers.

For those uncertain about immediate relocation, alternative strategies exist. Rent-back agreements, though not universally available, allow sellers to transfer ownership while continuing to occupy the home for a set period, often six months to a year, under a lease arrangement. This provides time to finalize community selection and move-in logistics without rushing the sale. Another option is a phased transition: moving into a short-term rental near a preferred retirement community to test the environment before committing financially. These approaches reduce pressure and allow for better alignment between housing proceeds and entry requirements.

Demographic shifts also influence timing. As the baby boomer generation ages, demand for senior housing is rising sharply. In many metropolitan areas, occupancy rates at reputable CCRCs exceed 90%, leading to longer waitlists and upward pressure on pricing. Communities with limited availability may raise entry fees or require larger deposits, particularly for desirable floor plans or priority access to healthcare services. Acting earlier—before demand intensifies further—can lock in today’s rates and secure placement ahead of future price increases. Waiting too long may mean settling for less ideal options or facing extended delays, especially in sought-after locations with mild climates or strong medical infrastructure.

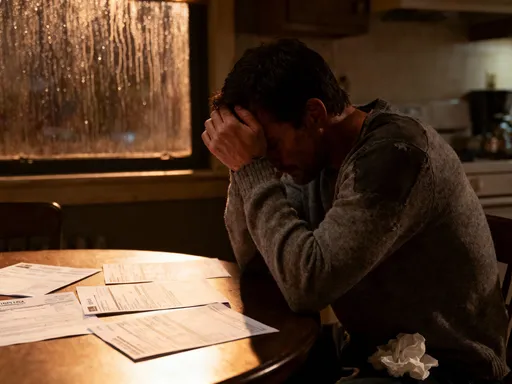

Protecting Your Nest Egg: Risk Management in Later Life

Safeguarding retirement savings is a top priority, and the structure of a retirement community contract can either reinforce or undermine that goal. Not all agreements are created equal—some offer greater financial protection than others. Refundable entry fee models, for example, allow a portion or all of the initial payment to be returned to the resident or estate upon departure, either through resale of the unit or direct reimbursement. This feature preserves capital and provides a safety net if circumstances change unexpectedly, such as improved health or family caregiving becoming viable. While these contracts often come with higher monthly fees, the trade-off can be worthwhile for those seeking asset protection.

Shared appreciation agreements represent another model, where the community gains a percentage of future home value increases in exchange for lower upfront costs. While this reduces initial outlay, it also limits long-term equity growth. Retirees must weigh the benefit of reduced entry barriers against the potential loss of wealth transfer to heirs. For those whose primary goal is comfort and care during life rather than estate maximization, this may be an acceptable compromise. Rental-based communities, meanwhile, eliminate large initial investments altogether, offering maximum flexibility. Though monthly costs may be higher and no equity is built, residents retain full control over their capital and can relocate more easily if needed.

Perhaps the greatest financial risk in later life is the need for extended long-term care. Traditional health insurance and Medicare do not cover custodial care, leaving families exposed to devastating costs. A well-structured retirement community contract that includes access to assisted living or skilled nursing at predetermined rates can mitigate this exposure. Without such protection, retirees may face market-rate nursing home bills that quickly deplete savings. By locking in care costs through a life-care agreement, individuals convert an unpredictable, potentially catastrophic expense into a known, manageable one. This is not merely convenience—it’s prudent financial planning.

It’s also important to consider inflation protection. Some contracts include escalation clauses tied to the Consumer Price Index or fixed annual increases, which help maintain service quality over time. Others do not, meaning future fee hikes could outpace income growth. Reviewing the historical rate of fee increases at a given community provides insight into affordability sustainability. Additionally, understanding what services are included—and what might incur extra charges—is vital. Unexpected costs for medication management, transportation, or specialized therapies can accumulate rapidly. Transparency in pricing and clear communication with administrators help prevent budget overruns and ensure long-term financial stability.

Lifestyle Inflation in Retirement: Are You Paying for Convenience?

Retirement often brings a desire for ease, comfort, and social connection—needs that retirement communities are designed to fulfill. Yet, this pursuit of convenience can lead to what economists call “lifestyle inflation”: spending more on non-essential comforts simply because they are available. Gourmet dining rooms, fitness centers, concierge services, and scheduled outings enhance daily life, but they also drive up monthly fees. The challenge lies in distinguishing between meaningful enrichment and unnecessary extravagance. Just as younger adults might overspend on subscriptions or dining out, retirees can unknowingly pay for amenities they rarely use.

Emotional attachment compounds the issue. After moving in, residents may feel invested—both financially and socially—in staying put, even as costs rise or needs change. This “lifestyle lock-in” effect makes it difficult to downsize or relocate, particularly when friendships form and routines settle. Some individuals remain in higher-cost independent living units long after they could benefit from assisted services, either due to pride, denial, or fear of disruption. Others hesitate to leave because they’ve paid non-refundable fees or worry about breaking contracts. These emotional and financial barriers can prevent optimal decision-making, leading to prolonged overspending.

To avoid this trap, it’s essential to evaluate usage patterns honestly. How often are meals eaten in communal dining halls versus prepared in-suite? Are fitness classes attended regularly, or does the pool go unused? Is transportation utilized for appointments, or does a personal vehicle still handle most trips? Tracking engagement with offered services helps determine whether the investment aligns with actual lifestyle. Communities that offer à la carte billing or tiered membership plans allow greater control over spending, letting residents pay only for what they use. Opting for a simpler floor plan or a more modest campus can also reduce costs without sacrificing core benefits.

Additionally, retirees should ask whether the location supports long-term goals. Is the community situated near family members who can visit or assist when needed? Does it offer access to quality external healthcare providers, pharmacies, and hospitals? Proximity to loved ones enhances emotional well-being and can reduce reliance on paid services. A vibrant social calendar means little if isolation persists due to lack of familial connection. Balancing convenience with practicality ensures that spending supports genuine well-being, not just momentary comfort. The goal is not austerity, but intentionality—designing a retirement lifestyle that delivers lasting value without straining resources.

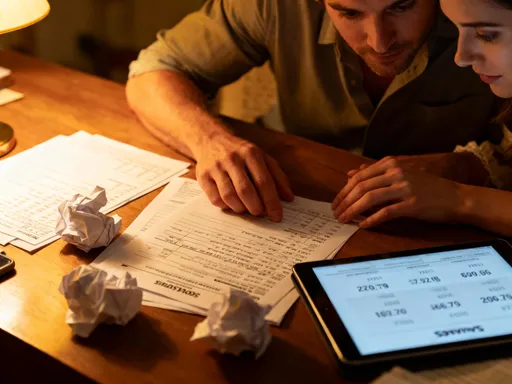

The Tax and Estate Planning Angle: Silent Gains You Can’t Ignore

Relocating to a retirement community isn’t just a housing decision—it’s a financial event with tax and estate implications that, when managed wisely, can yield significant advantages. One of the most impactful benefits arises from the sale of a primary residence. Under current U.S. tax law, individuals can exclude up to $250,000 in capital gains from taxation, or $500,000 for married couples filing jointly, provided they’ve lived in the home for at least two of the past five years. This exemption can preserve tens or even hundreds of thousands of dollars that would otherwise go to the IRS, effectively increasing the pool of funds available for community entry. Timing the sale to maximize this benefit—ideally before any rental use or prolonged absence—is crucial.

From an estate planning perspective, moving into a community can simplify asset distribution and reduce administrative complexity. Holding real estate in a single-family home introduces challenges: property management, potential disputes among heirs, and probate delays. Transferring equity into a retirement community contract, particularly one with a refundable component, can streamline inheritance. Some contracts allow designated beneficiaries to receive a portion of the entry fee upon the resident’s passing, reducing the burden on executors and ensuring faster access to funds. Gifting strategies can also play a role; parents may choose to transfer proceeds directly to children to reduce taxable estate size or fund grandchild education, though such moves require careful coordination with legal and tax advisors.

Medicaid eligibility is another consideration, though it varies by state and contract type. Most retirement communities are private-pay and do not accept Medicaid, but some have skilled nursing wings that do. For individuals concerned about qualifying for government assistance in the future, the timing and structure of asset transfers matter greatly. Transferring assets too close to a Medicaid application can trigger penalty periods, so advance planning—often five years or more ahead—is recommended. Consulting with an elder law attorney ensures compliance with rules while protecting financial interests. Importantly, prepaid life-care contracts are generally not counted as countable assets for Medicaid purposes, offering a legitimate way to allocate funds toward future care without jeopardizing eligibility.

Additionally, property tax relief may be available after selling a home, especially for seniors who previously qualified for homestead exemptions or age-based reductions. While these savings won’t cover community fees, they can contribute to overall cash flow. Charitable remainder trusts and qualified personal residence trusts are advanced tools that some retirees use to defer taxes or transfer real estate efficiently, though they require professional guidance. Ultimately, integrating the move into a broader financial plan—rather than treating it in isolation—unlocks hidden efficiencies and ensures that every dollar serves a purpose.

Making the Call: Signs It’s Time to Act—And When to Wait

There is no universal timeline for moving into a retirement community. The right moment depends on a confluence of financial, health, emotional, and logistical factors. Clear green lights include consistent income coverage of projected fees, growing difficulty maintaining the current home, proximity to quality healthcare, and strong interest in social engagement. When family members express concern about safety—such as falls, forgotten medications, or isolation—it’s often a signal that change is overdue. Similarly, if home repairs have become frequent or overwhelming, or if winter snow removal poses a physical risk, the case for transition strengthens. Geographic desires also matter; many retirees choose to relocate closer to adult children or to regions with milder climates, better air quality, or lower living costs.

Red flags suggest waiting may be wiser. If market conditions are unfavorable and selling now would mean accepting a low offer, it may be better to delay. Similarly, if health is rapidly declining and immediate skilled nursing is likely, a traditional CCRC may not be the most efficient path—direct admission to a nursing facility might be more appropriate. Emotional unreadiness is another valid reason to pause. Some individuals resist leaving a long-time home due to sentimental attachment or fear of the unknown. Pressuring them can lead to resentment or poor adjustment. Instead, visiting communities together, attending events, and allowing time for exploration can ease the transition.

A balanced approach involves scenario planning. Projecting expenses over 10, 15, or 20 years under different models—staying put, downsizing, or moving to a community—helps compare outcomes. Stress-testing assumptions, such as lower investment returns or higher-than-expected fee increases, reveals vulnerabilities. Consulting a fee-only financial planner with experience in senior transitions adds objectivity and depth to the analysis. The goal is not to chase perfection, but to make a decision grounded in facts, values, and long-term well-being.

In the end, the best time to invest in a retirement community is when it enhances both financial security and quality of life. It’s not about age, but alignment—between resources and needs, independence and support, comfort and sustainability. With thoughtful planning, this move can be one of the most empowering financial decisions of later life, offering peace of mind not just for the individual, but for the entire family.