How I Navigated Financial Chaos After an Accident — A Real Market Insight Guide

I never thought a sudden accident would shake my finances until it happened to me. Overnight, medical bills piled up and income stalled. What saved me wasn’t luck — it was understanding how markets shift during crises and making smart, quick moves. In this guide, I’ll walk you through the real steps I took, from emergency funds to strategic investments, showing how market awareness can protect your money when disaster strikes. This isn’t a story of overnight riches or risky gambles. It’s about practical, grounded decisions rooted in financial discipline and long-term thinking. If you’ve ever feared how a single unexpected event could unravel your stability, this is for you. The truth is, most of us are one incident away from financial strain. But with the right tools and mindset, even the worst moments can become catalysts for smarter money management.

When Life Crashes: The Hidden Financial Impact of Accidents

Accidents are not just physical events — they are financial earthquakes. When a car crash left me unable to work for three months, I quickly realized that the injury was only half the battle. The other half was the avalanche of financial stress that followed. My monthly income vanished almost overnight, yet my expenses did not. Rent, groceries, utilities, and insurance premiums continued as if nothing had changed. What made it worse was the sudden surge in medical costs — hospital visits, physical therapy, prescription medications — none of which were fully covered by insurance. Within weeks, I was staring at a growing deficit, and the emotional toll began to cloud my judgment. I considered taking out a high-interest personal loan, a decision I now recognize as potentially disastrous.

What I didn’t understand at the time was how common this scenario is. Millions of households face similar shocks every year, not because of poor financial habits, but because life is unpredictable. According to data from the Federal Reserve, nearly 30% of Americans would struggle to cover an unexpected $400 expense without borrowing or selling something. This statistic reveals a deeper truth: financial fragility is not limited to low-income families. Even middle-class households with steady jobs can be unprepared for sudden disruptions. The core issue is not spending too much or saving too little in normal times — it’s the lack of a structured response plan when income stops and costs spike simultaneously.

The psychological impact of financial stress after an accident cannot be overstated. Anxiety about money can impair decision-making, leading individuals to make short-term choices that harm long-term stability. For example, selling investments at a market low to cover medical bills locks in losses and delays recovery. Similarly, relying on credit cards to manage cash flow can result in compounding debt that takes years to repay. These reactions are understandable, but they are also avoidable with proper preparation. The key is recognizing that financial resilience is not about having perfect timing or insider knowledge — it’s about having systems in place before disaster strikes. This means more than just budgeting; it requires a holistic approach that includes liquidity, insurance, and market awareness.

My experience taught me that the true cost of an accident extends far beyond medical bills. It includes lost wages, reduced earning capacity, and the long-term consequences of financial strain. For many, the recovery period is not just physical but economic. It can take months or even years to regain financial footing, especially if assets are liquidated or debt is accumulated. The good news is that this cycle can be broken. By understanding the typical financial trajectory after an accident — the sudden drop in income, the spike in expenses, and the emotional pressure — individuals can begin to build safeguards. These safeguards are not luxury items for the wealthy; they are essential tools for anyone who values stability and peace of mind. The first step is acknowledging that financial risk is not just about market volatility — it’s also about life’s unpredictability.

Reading the Market Pulse: Why Crises Change Investment Landscapes

When I was recovering from my accident, I made a habit of reviewing my investment portfolio every few weeks. At first, I considered selling everything to access cash. But instead of acting on impulse, I decided to study how markets were responding to broader economic conditions. What I discovered changed my perspective. Crises — whether health-related, economic, or natural — don’t affect all industries equally. Some sectors decline, while others experience increased demand. For example, during periods of public health stress, healthcare technology, telemedicine, and medical equipment companies often see rising interest from investors. At the same time, travel, hospitality, and luxury goods tend to underperform. Recognizing these patterns allowed me to avoid panic-driven decisions and instead position my investments more strategically.

Market movements during crises are not random. They reflect shifts in consumer behavior, government policy, and supply chain dynamics. When accidents or health emergencies become widespread, investor sentiment shifts toward defensive assets — those that are more likely to maintain value during downturns. These include utilities, consumer staples, and certain healthcare stocks. Conversely, cyclical sectors like manufacturing and real estate may experience volatility. By observing these trends rather than reacting emotionally, investors can adjust their portfolios to reduce risk without abandoning long-term goals. This doesn’t mean timing the market perfectly — that’s nearly impossible — but it does mean being informed enough to avoid costly mistakes.

One of the most valuable lessons I learned was the importance of staying engaged with financial news, even during personal hardship. I began reading reliable financial reports and tracking sector performance, not to make speculative trades, but to understand the bigger picture. For instance, I noticed that insurance companies were adjusting their risk models in response to increased claims, which affected their stock valuations. At the same time, digital health platforms were expanding rapidly, driven by greater demand for remote care. This insight didn’t lead me to invest heavily in any single stock, but it did help me rebalance my portfolio toward more stable, resilient industries. I shifted a portion of my holdings from high-growth tech stocks — which were volatile at the time — into dividend-paying healthcare and utility companies.

What this taught me is that financial resilience isn’t just about having money saved — it’s also about understanding how money moves. Markets are not abstract entities; they respond to real-world events. When accidents or health crises increase, certain economic patterns emerge. Investors who pay attention can use this information to protect their wealth. For example, during a period of economic uncertainty, bond yields may rise as investors seek safety, making fixed-income investments more attractive. Similarly, commodities like gold often serve as hedges against inflation and market instability. None of these strategies guarantee profits, but they do offer ways to reduce exposure to unnecessary risk. The goal is not to become a market expert overnight, but to develop a habit of observation and thoughtful adjustment.

Emergency Fund or Bust: Building Your First Line of Defense

If there’s one financial tool that saved me during my recovery, it was my emergency fund. Before the accident, I had built a reserve equal to six months of essential living expenses. At the time, it felt like a lot of money sitting idle. I often questioned whether I should invest it instead. But when my income stopped, that fund became my lifeline. It covered rent, groceries, insurance, and even some medical co-pays without forcing me to take on debt. More importantly, it gave me time — time to heal, time to assess my situation, and time to make thoughtful financial decisions instead of desperate ones. The presence of that fund reduced my stress significantly and prevented me from making irreversible mistakes.

Building an emergency fund is not complicated, but it does require discipline. The general rule is to save enough to cover three to six months of basic expenses — housing, food, utilities, transportation, and insurance. For someone with a variable income or greater financial responsibilities, such as a single parent or self-employed individual, a larger buffer may be necessary. The key is to define what “essential” means in your life and calculate accordingly. Once you have a target amount, set up automatic transfers from your checking account to a separate savings account each payday. Treat this transfer like a non-negotiable bill. Over time, even small contributions add up. For example, saving $200 a month will yield $12,000 in five years — a substantial cushion for most emergencies.

Where you keep your emergency fund matters as much as how much you save. It should be in a safe, liquid account that allows quick access without penalties. A high-yield savings account is often the best choice — it offers better interest than a traditional bank while keeping your money readily available. Avoid tying this fund to investments like stocks or mutual funds, which can lose value when you need the money most. Similarly, do not use retirement accounts as emergency reserves; early withdrawals usually come with taxes and penalties. The purpose of this fund is stability, not growth. It’s not meant to generate wealth — it’s meant to preserve it during difficult times.

One of the biggest challenges with emergency funds is resisting the temptation to dip into them for non-emergencies. It’s easy to justify using the money for a vacation, a home renovation, or even a “great investment opportunity.” But doing so undermines its purpose. To maintain discipline, establish clear rules for withdrawals — for example, only in cases of job loss, medical crisis, or essential home repair. You might even give your account a label like “Do Not Touch — Financial Safety Net” to reinforce its importance. Remember, the true value of an emergency fund is not measured in interest earned, but in peace of mind gained. It’s the foundation of financial resilience, and without it, even minor setbacks can become major crises.

Protecting Assets: Insurance That Actually Works When You Need It

During my recovery, I quickly learned that not all insurance is created equal. While my health insurance covered a significant portion of my hospital bills, it left gaps — particularly for outpatient care, physical therapy, and prescription drugs. I also discovered that my standard disability insurance policy had a 90-day waiting period before benefits kicked in, which meant I received no income replacement during the first three months of my recovery. This gap could have been devastating if not for my emergency fund. The experience taught me that having insurance is not the same as being protected. What matters is whether the policy delivers meaningful benefits when you need them most.

There are several types of insurance that can provide real protection in the event of an accident. Health insurance is essential, but it’s not enough on its own. Disability insurance, which replaces a portion of your income if you’re unable to work, is a critical layer of defense. However, not all policies are the same. Short-term disability typically covers three to six months and has a shorter waiting period, while long-term disability can provide benefits for years or even until retirement. It’s important to understand the terms — including the elimination period (the waiting time before payments begin), the benefit amount, and what qualifies as a disability. Some policies exclude pre-existing conditions or certain types of injuries, so read the fine print carefully.

Critical illness and accident insurance are additional options worth considering. These policies pay a lump sum if you’re diagnosed with a covered condition or suffer a qualifying injury. The money can be used for anything — medical bills, living expenses, or even travel for treatment. Unlike traditional health insurance, which pays providers directly, these policies give you cash to manage as you see fit. While they come with premiums, the payout can be a game-changer during a financial crisis. For example, a $10,000 benefit from an accident policy could cover several months of rent or prevent the need to withdraw from retirement savings.

When evaluating insurance, focus on the benefits, not just the cost. A low-premium policy may seem attractive, but if it denies claims or has restrictive terms, it offers little value. Look for policies with clear eligibility criteria, reasonable waiting periods, and strong customer reviews. If you’re employed, check what coverage your employer offers and consider supplementing it with individual policies. And always keep documentation of medical records and claims organized — this can speed up the approval process when time is critical. Insurance is not a one-time decision; it should be reviewed regularly to ensure it aligns with your current life situation. The goal is not to have the cheapest policy, but the one that truly protects you when life goes off track.

Smart Moves in a Downturn: Tactical Investing After a Crisis

One of the most dangerous financial impulses during a crisis is the urge to sell everything and move to cash. I felt that pressure strongly when my accident happened. With no income and mounting bills, I considered liquidating my investment accounts to free up money. But I paused and reminded myself of a fundamental principle: markets go down, but they also recover. Selling during a downturn locks in losses and removes the opportunity to benefit from future growth. Instead of panicking, I chose to rebalance my portfolio based on my long-term goals and risk tolerance. This decision preserved my capital and positioned me for recovery when markets stabilized.

Tactical investing during a crisis doesn’t mean chasing hot stocks or making speculative bets. It means making thoughtful adjustments to protect your wealth. One strategy I used was shifting toward defensive assets — investments that tend to hold their value even when the economy is weak. These include dividend-paying stocks in stable industries like healthcare, consumer staples, and utilities. While they may not offer explosive growth, they provide income and relative safety. I also increased my allocation to bonds, particularly high-quality government and corporate bonds, which tend to be less volatile than stocks. This didn’t eliminate risk, but it reduced my exposure to sharp market swings.

Another smart move was identifying undervalued sectors with strong recovery potential. For example, I noticed that medical technology and telehealth companies were innovating rapidly in response to increased demand. While I didn’t invest heavily, I did allocate a small portion of my portfolio to exchange-traded funds (ETFs) focused on healthcare innovation. This allowed me to participate in potential growth without taking on excessive risk. The key was diversification — spreading investments across different asset classes and sectors to avoid overexposure to any single risk. Diversification doesn’t guarantee profits, but it does reduce the impact of any one loss.

Rebalancing is another essential practice. Over time, market movements can shift your portfolio’s original allocation. For instance, if stocks perform well, they may grow to represent a larger share of your holdings than intended, increasing your risk. Rebalancing means selling some of the overperforming assets and buying more of the underperforming ones to return to your target mix. I did this annually, even during my recovery, to maintain alignment with my long-term strategy. It’s a disciplined approach that prevents emotional decision-making and keeps your investments on track. The goal isn’t to time the market, but to stay invested in a way that reflects your goals and risk tolerance.

Cutting Costs Without Sacrificing Security: Budgeting Under Pressure

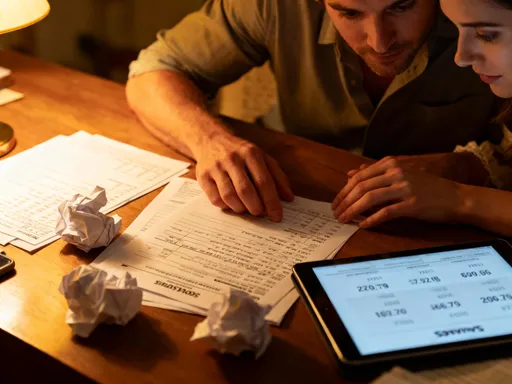

When income drops, expenses must be scrutinized. During my recovery, I created a crisis budget that distinguished between essential and discretionary spending. Essentials — rent, food, utilities, insurance, and medical costs — were non-negotiable. Everything else was evaluated. I canceled subscription services I wasn’t using, paused contributions to non-retirement investment accounts, and postponed home maintenance projects that weren’t urgent. I also contacted my service providers — internet, phone, insurance — to negotiate lower rates or temporary relief. These adjustments freed up hundreds of dollars each month, which I redirected toward medical co-pays and daily living costs.

Budgeting under pressure is not about deprivation — it’s about prioritization. The goal is to preserve financial stability without compromising health or long-term security. For example, I continued paying my retirement contributions at a reduced level rather than stopping them completely. This allowed me to maintain the habit of saving and avoid penalties for early withdrawal. I also avoided high-interest debt by using my emergency fund instead of credit cards. While it was tempting to put medical bills on a card with a 0% introductory rate, I knew that if I couldn’t pay it off before the rate increased, I’d be trapped in a cycle of debt.

Another helpful strategy was leveraging community resources. I discovered that local health clinics offered discounted physical therapy, and some pharmaceutical companies provided assistance programs for prescription medications. Nonprofit organizations and government programs also offered support for utility bills and food expenses. These resources didn’t solve everything, but they reduced the burden significantly. I also reached out to family and friends for emotional and practical support, which helped me avoid making impulsive financial decisions out of stress.

The discipline of crisis budgeting taught me that financial resilience is not just about how much you earn, but how you manage what you have. By cutting non-essentials, negotiating bills, and using available resources, I extended the life of my emergency fund and avoided debt. This breathing room gave me the space to focus on recovery rather than financial panic. Once my income resumed, I gradually restored my previous spending levels, but I kept many of the frugal habits I had developed. These changes became permanent improvements to my financial health.

Rebuilding Stronger: Turning Trauma into Financial Resilience

Recovery is not just about healing the body — it’s about rebuilding financial strength. Once I returned to work, I didn’t simply resume my old financial habits. I used the experience as a catalyst for lasting change. I increased my emergency fund from six to nine months of expenses, updated my insurance coverage to close the gaps I had discovered, and revised my investment strategy to include more defensive assets. I also created a personal financial contingency plan — a written document outlining what to do in various emergency scenarios, from job loss to medical crisis. This plan includes contact information for insurers, steps for accessing funds, and a list of essential expenses.

One of the most important changes was adopting a mindset of proactive preparedness. I now review my financial situation quarterly, not just annually. I monitor market trends, reassess my risk tolerance, and ensure my estate plan — including wills and beneficiary designations — is up to date. I also educate myself continuously, reading reputable financial publications and consulting with a fee-only financial advisor when needed. Knowledge is power, and the more I understand about money, the more confident I feel in my ability to handle future challenges.

Financial resilience is not built overnight. It’s the result of consistent habits, informed decisions, and a willingness to learn from experience. My accident was a painful event, but it also became a powerful teacher. It showed me that wealth is not just about accumulating assets — it’s about protecting them. It’s not just about earning money — it’s about managing it wisely, especially when life doesn’t go as planned. Today, I feel more secure not because I have more money, but because I have better systems in place. And if another crisis comes, I know I’ll be ready. The goal is not to fear the unexpected, but to prepare for it — because true financial peace comes not from avoiding risk, but from being prepared to face it with confidence.