How I Mastered Financial Planning Without Losing My Mind

Ever feel like your budget vanishes before month-end? I’ve been there—stressed, overspending, and clueless about where my money went. After years of trial and error, I discovered advanced cost control methods that actually work. It’s not about cutting coffee runs; it’s smarter planning. This is my journey from chaos to control, sharing real strategies that reshaped my finances—and can transform yours too.

The Wake-Up Call: When My Budget Blew Up

It happened on a Tuesday morning, like so many financial crises do—not with a bang, but with a sinking feeling as I opened my bank app. My paycheck had cleared the day before, yet my checking account balance hovered just above zero. There was no major purchase to explain it, no emergency expense, no sudden bill. Just a slow, silent erosion of funds that left me confused and anxious. I had a stable job, health benefits, and no debt beyond a manageable mortgage. On paper, I was doing fine. In reality, I was living paycheck to paycheck, one missed payment away from stress-induced insomnia. That moment was my wake-up call—the realization that my financial habits, though not reckless, were fundamentally unsustainable.

Looking back, the warning signs had been there for years. I’d been budgeting in the most basic sense: setting a monthly limit on groceries or entertainment, then crossing my fingers. But I never tracked where the money actually went. I assumed I was being careful, yet I couldn’t explain why I was always short. The truth was, I didn’t understand my spending patterns. I made impulse buys during lunch breaks, upgraded subscriptions without evaluating their value, and treated occasional expenses—like car maintenance or gifts—as surprises, even though they occurred every year. My budget wasn’t broken because I earned too little; it was broken because I planned too little.

What made this moment different was the emotional toll. It wasn’t just about the numbers. It was the constant low-grade anxiety that came with financial uncertainty—the dread of checking my account, the guilt after an unplanned purchase, the frustration of setting savings goals I never reached. I realized that if I didn’t change my approach, I’d stay stuck in this cycle indefinitely. I needed more than a spreadsheet. I needed a system. That’s when I began researching advanced cost control methods—strategies that go beyond basic budgeting to create sustainable financial stability. This wasn’t about deprivation; it was about design. And it started with a single question: where was my money really going?

Beyond Budgeting: Rethinking Cost Control

Most people think of budgeting as a list of income and expenses, a rigid framework that tells you what you can and can’t spend. But I learned that real financial control isn’t about restriction—it’s about intention. Cost control, at its core, is proactive financial design. It’s not just tracking where money goes, but shaping how and when it flows. This shift in mindset changed everything. Instead of asking, “Can I afford this?” I began asking, “Does this align with my goals?” That subtle difference transformed spending from a source of guilt into a tool for progress.

One of the first changes I made was reevaluating recurring expenses. I had subscriptions to three streaming services, two meal-kit deliveries I rarely used, and a premium cloud storage plan I didn’t need. Individually, each seemed minor—$10 here, $15 there. But together, they amounted to over $120 a month, more than $1,400 a year. I canceled two subscriptions immediately and downgraded the third. The savings weren’t life-changing on their own, but they represented a pattern: small, automatic outflows that accumulated silently. By addressing them, I reclaimed control over my cash flow.

Another key strategy was renegotiating fixed bills. I called my internet provider and asked for a better rate, citing competitor offers. To my surprise, they matched the price without requiring a contract. I did the same with my car insurance, shopping around and switching to a provider that offered a lower premium for the same coverage. These actions required minimal effort but yielded significant results—over $800 in annual savings. What mattered most wasn’t the money saved, but the realization that many costs aren’t fixed. They’re negotiable, especially if you’re willing to spend a few minutes each year reviewing them.

This approach to cost control isn’t about cutting everything. It’s about optimizing. It’s understanding that every dollar has potential—either as a leak or an investment. When I began viewing expenses through this lens, I stopped seeing financial discipline as a burden and started seeing it as empowerment. I wasn’t giving up things I loved; I was redirecting resources toward what truly mattered. That shift in perspective made the entire process sustainable, even motivating.

The Hidden Leaks: Tracking What Really Matters

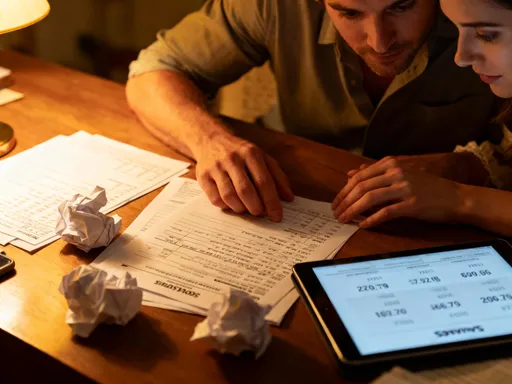

Even with a budget in place, money was still disappearing. I knew I hadn’t made any big purchases, yet my account balance dwindled faster than expected. That’s when I decided to conduct a full financial audit—a 90-day review of every transaction. I downloaded my bank statements, imported them into a simple spreadsheet, and categorized each expense. What I discovered was eye-opening. The biggest drains weren’t groceries or gas or even dining out. They were the small, automatic payments I barely noticed: app subscriptions, bank fees, forgotten memberships, and duplicate services. These hidden leaks accounted for nearly 18% of my monthly spending.

Lifestyle creep was another silent thief. Over the years, I had gradually upgraded my habits—premium coffee instead of home brew, delivery apps instead of cooking, boutique fitness classes instead of walking. These weren’t luxuries I planned for; they were incremental changes that became routine. Alone, each seemed insignificant. Together, they created a spending baseline I hadn’t consciously chosen. I also uncovered emotional spending patterns—times when stress or boredom triggered unplanned purchases. A rough day at work often ended with an online shopping spree, disguised as self-care. These behaviors weren’t reckless, but they were automatic, and they undermined my financial progress.

Tracking didn’t come naturally at first. It felt tedious, even obsessive. But over time, it became empowering. I wasn’t just recording numbers; I was gaining insight. I learned that I spent more on weekends, that certain apps triggered impulse buys, and that I was more likely to overspend when tired or overwhelmed. This awareness allowed me to make informed adjustments. I canceled unused subscriptions, set up alerts for recurring charges, and introduced a 24-hour waiting period for non-essential purchases. I also started using a cash envelope system for discretionary categories, which made spending more tangible and limited overuse.

The key wasn’t perfection. I didn’t eliminate all leaks, nor did I expect to. The goal was consistency—building a habit of awareness. Over time, tracking became less about scrutiny and more about clarity. I no longer felt blind-sided by my spending. I could anticipate expenses, adjust in real time, and make choices aligned with my priorities. This shift didn’t require willpower; it required visibility. And once I could see where my money was going, I could finally take control.

Building Financial Guardrails: Systems That Work

Willpower is unreliable. No matter how motivated I felt on a Monday, by Friday, stress or fatigue could undo my best intentions. That’s why I stopped relying on discipline alone and built systems—financial guardrails that enforced good habits automatically. These weren’t restrictions; they were safeguards designed to protect my progress without demanding constant vigilance. The goal was to make smart financial behavior the default, not the exception.

One of the most effective systems I implemented was payment delay. Instead of paying bills or making purchases immediately, I set up a 48-hour cooling-off period for any non-essential transaction. I moved my primary spending account to an online bank with slightly slower transfers, which created natural friction. This small delay didn’t stop me from buying things I truly wanted, but it eliminated impulse purchases. I found that if I still wanted an item two days later, it was usually worth buying. If not, I saved the money without regret.

I also introduced spending thresholds. For categories like dining out, shopping, and entertainment, I set monthly limits based on historical data and financial goals. Once a category reached 80% of its limit, I received an alert. At 100%, the funds were no longer accessible—either because I had moved the money to a separate account or because I used a debit card with customizable controls. This wasn’t about punishment; it was about accountability. It allowed me to enjoy life while staying within boundaries.

Automation played a crucial role. I set up automatic transfers to savings and investment accounts on payday, ensuring that I paid myself first. I also automated bill payments to avoid late fees and credit damage. But I went further—I automated limits on discretionary spending. Using a financial app with envelope-style budgeting, I allocated funds to different categories at the start of each month. Once a category was depleted, I couldn’t overspend without manually moving money from another category, which required conscious effort. This system didn’t eliminate spending; it made it intentional. Over time, these guardrails became invisible, yet their impact was profound. I stopped worrying about overspending because the system made it nearly impossible.

Aligning Costs with Goals: Planning with Purpose

Financial discipline feels punishing when it’s disconnected from meaning. I learned this the hard way when I tried to cut every non-essential expense in the name of saving. I lasted six weeks before burning out and making a series of rebound purchases. That experience taught me a critical lesson: sustainable cost control must be rooted in purpose. Every dollar saved should serve a goal, and every expense should reflect a value.

I began by defining my financial priorities. First came the emergency fund—three to six months of living expenses set aside for unexpected events. I treated this as non-negotiable, like a utility bill. Once that was established, I focused on debt reduction, targeting my highest-interest obligations first. Only then did I turn to investing, starting with a retirement account and gradually expanding to other vehicles. By ranking these goals, I created a clear roadmap. Every financial decision could be measured against it: did this action move me closer to stability, or further away?

This framework transformed my relationship with money. Instead of feeling guilty for spending, I felt empowered when I aligned my choices with my objectives. I still dined out, traveled, and bought clothes—but now, those expenses were planned and purposeful. I budgeted for them in advance, knowing they were part of a balanced life. I also began to view spending as a form of self-investment. A cooking class, for example, wasn’t just entertainment; it was a way to save on dining out long-term. A reliable laptop wasn’t a luxury; it was a tool for career growth. This shift in perspective reduced internal conflict and made financial planning feel less like restriction and more like strategy.

Perhaps the most powerful change was emotional. When I spent with intention, I enjoyed it more. There was no lingering guilt, no second-guessing. I had given myself permission, because the spending fit within a larger plan. This alignment between action and values created a sense of integrity—one of the most overlooked benefits of financial health. Money stopped being a source of stress and started being a tool for building the life I wanted.

Risk and Reality: Avoiding the Overcorrection Trap

One of the biggest dangers in financial planning is overcorrection. In my early attempts to gain control, I cut too deeply, eliminating all leisure spending, social activities, and small pleasures. I thought discipline meant denial. Within two months, I was exhausted, resentful, and craving release. The result? A weekend shopping spree that wiped out two months of savings. I had fallen into the deprivation-rebound cycle—a common trap where extreme frugality leads to burnout and overspending.

This experience taught me that risk management in personal finance isn’t just about protecting your net worth. It’s about protecting your well-being. A sustainable plan must include flexibility, room for error, and space for joy. I realized that financial health isn’t measured solely by account balances, but by peace of mind. If a budget causes constant stress, it’s not working—even if it looks perfect on paper.

I revised my approach to include what I call “guilt-free spending.” Each month, I allocate a small portion of my budget—about 5%—to discretionary use with no questions asked. Whether it’s a new book, a coffee treat, or a spontaneous gift, this fund allows me to enjoy life without derailing my goals. I also built in seasonal flexibility. During holidays or family events, I adjust categories to accommodate higher spending, knowing I’ve planned for it in advance. This doesn’t mean abandoning discipline; it means practicing it with compassion.

The goal is balance. I no longer aim for perfection. I aim for progress. I accept that I’ll make mistakes, that some months will be tighter than others, and that unexpected expenses will arise. What matters is having a system that absorbs those shocks without collapsing. By designing a plan that includes both structure and flexibility, I’ve created a financial life that’s not just sustainable, but livable.

The Payoff: Gaining More Than Just Savings

Looking back, the greatest benefit of mastering financial planning wasn’t the money I saved—it was the freedom I gained. I no longer dread opening my bank app. I make decisions with confidence, knowing I have a plan and the tools to follow it. The constant background stress has faded, replaced by a quiet sense of control. I sleep better. I worry less. I enjoy my spending more because it’s intentional, not impulsive.

This journey wasn’t about getting rich. It was about getting clear. By implementing advanced cost control methods—tracking hidden leaks, building guardrails, aligning spending with goals—I transformed my relationship with money. I stopped seeing it as a source of anxiety and started seeing it as a reflection of my choices. Every dollar became a vote for the life I wanted to live.

I share these strategies not because I’m perfect, but because I’ve been where you might be—overwhelmed, uncertain, and ready for change. The methods I’ve described are practical, tested, and designed for real life. They don’t require extreme sacrifice or complex financial knowledge. They require awareness, consistency, and a willingness to plan with purpose. If you’re tired of living paycheck to paycheck, if you want to stop wondering where your money went, if you crave stability without losing your joy—this is possible. Financial control isn’t about restriction. It’s about empowerment. And it starts with a single step: deciding that your peace of mind is worth the effort.